Canada Freight Brokerage Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

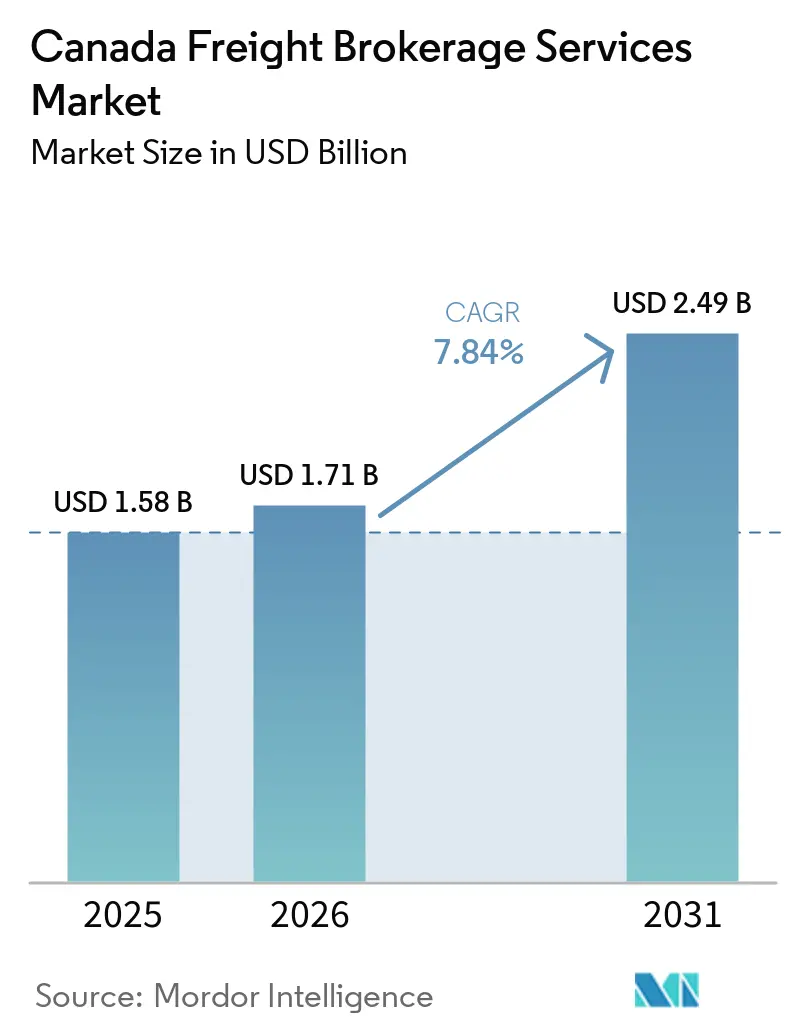

| Base Year Market Size (2025) | USD 1.58 Billion |

| Market Size (2026) | USD 1.71 Billion |

| Market Size (2031) | USD 2.49 Billion |

| Growth Rate (2026 - 2031) | 7.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ����������. Reuse requires attribution under CC BY 4.0. | |

Canada Freight Brokerage Services Market Analysis by ����������

The Canada freight brokerage services market size is projected to be USD 1.58 billion in 2025, USD 1.71 billion in 2026, and reach USD 2.49 billion by 2031, growing at a CAGR of 7.84% from 2026 to 2031. Steady recovery in automotive production, accelerated federal infrastructure upgrades, and the Canada Border Services Agency’s (CBSA) digital customs program are expanding cross-border freight volumes, favoring intermediary coordination. Investments from the National Trade Corridors Fund (NTCF) are removing long-standing capacity bottlenecks on key rail and port corridors, reducing transit-time variability and boosting carrier asset turns. Retailers are demanding API-enabled, real-time visibility, compelling brokers to deploy machine-learning tools that predict ETAs and manage exceptions. At the same time, Health Canada’s tightened cold-chain rules for pharmaceuticals are lifting demand for temperature-controlled capacity that commands premium brokerage margins. These converging drivers are expanding the addressable pool of shippers who view technology-capable brokers as strategic supply-chain partners rather than transactional load finders.[1]Health Canada, “Good Distribution Practices Guide for Drugs,” canada.ca

Key Report Takeaways

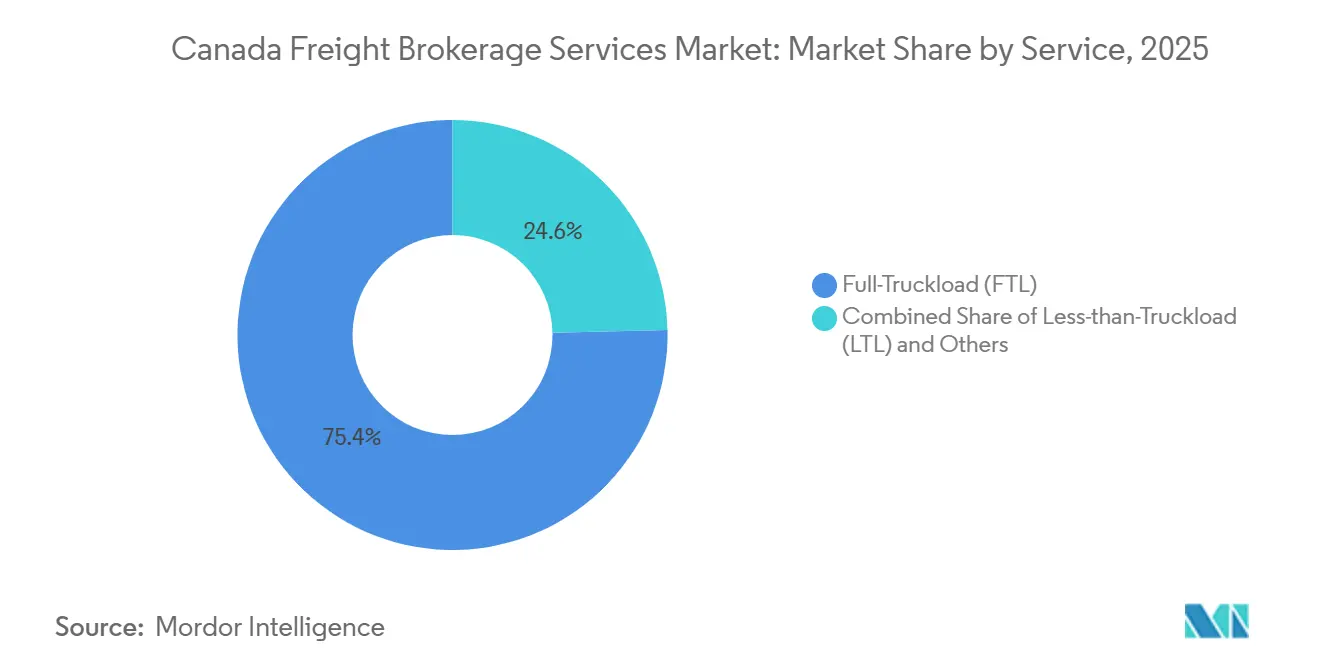

- By service line, full-truckload brokerage led with 75.37% revenue share in 2025, while less-than-truckload is projected to advance at a 9.45% CAGR through 2031.

- By equipment type, dry-van movements accounted for 40.79% of the Canada freight brokerage services market share in 2025; refrigerated vans are forecast to grow at a 9.73% CAGR through 2031.

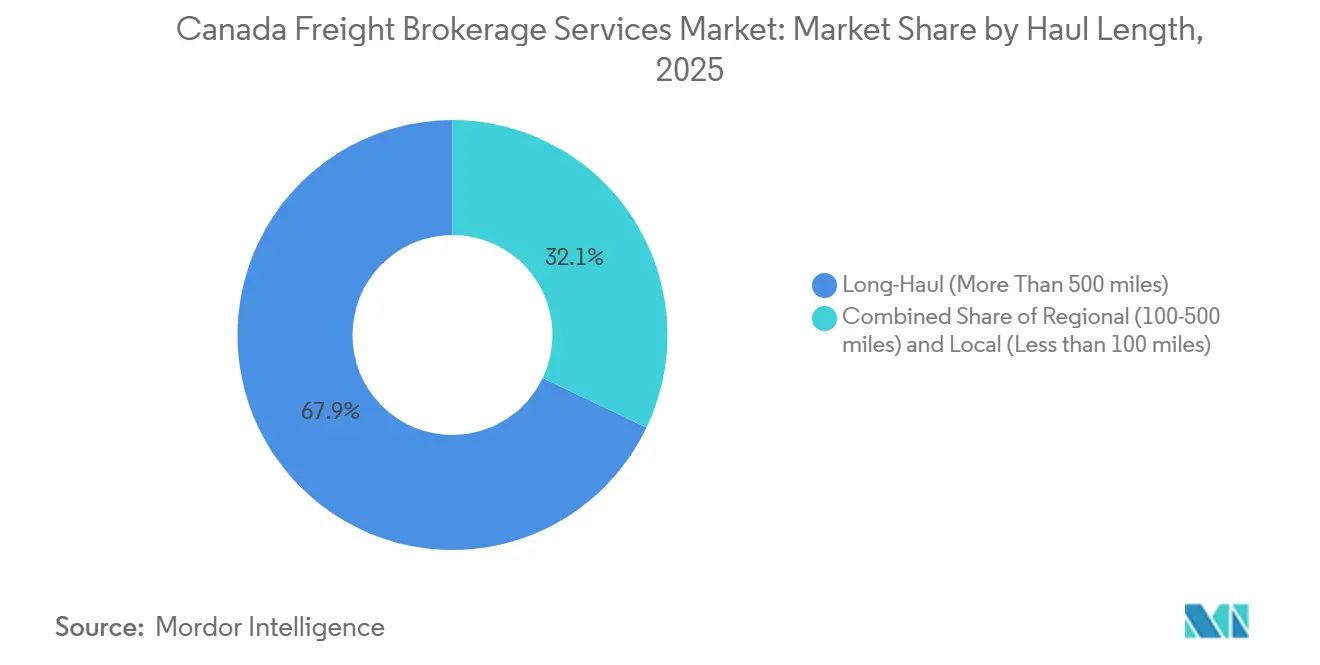

- By haul length, long-haul lanes held 67.92% share in 2025, whereas local shipments below 100 miles are expanding at an 11.78% CAGR to 2031.

- By business model, traditional brokerage accounted for 78.30% of 2025 revenue; digital platforms are projected to grow at a 27.09% CAGR by 2031.

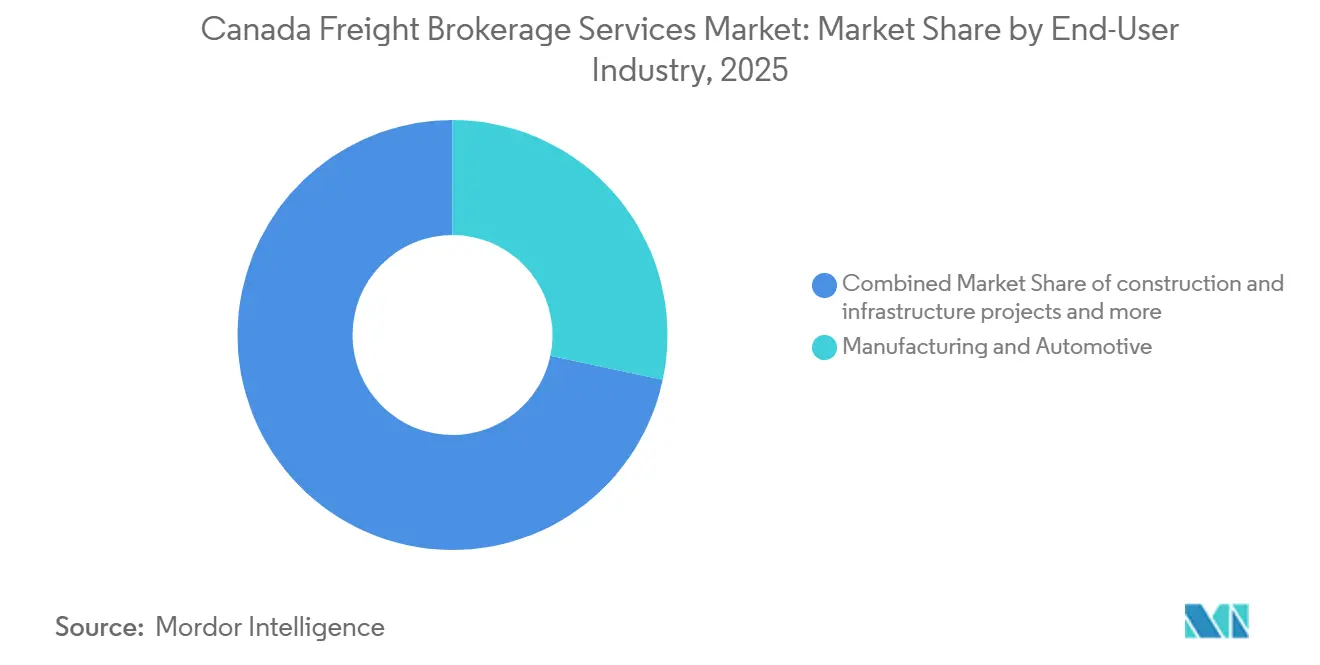

- By end-user industry, manufacturing and automotive accounted for 28.33% of 2025 turnover, while the e-commerce and 3PL fulfillment segment is set to grow at a 20.15% CAGR through 2031.

- By customer size, large enterprises contributed 68.09% of 2025 load volume, but small businesses below USD 10 million are pacing at a 14.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ����������’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada contributes to a system defined not by any single country or region but by the interaction of many. The global freight brokerage services market data by ���������� represents that combined structure.

Canada Freight Brokerage Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive-production rebound boosting inbound parts flows | +1.9% | Ontario, Quebec manufacturing corridors | Short term (≤ 2 years) |

| National Trade Corridors Fund upgrades expanding freight capacity | +1.6% | National, focus on British Columbia and Ontario gateways | Medium term (2-4 years) |

| Cross-border e-commerce returns surge fueling reverse-logistics lanes | +1.4% | Ontario, Quebec, British Columbia border regions | Medium term (2-4 years) |

| Retail-mandated real-time visibility APIs accelerating tech adoption | +1.2% | Major metros nationwide | Long term (≥ 4 years) |

| CBSA CARM Phase-2 rollout spurring demand for compliant brokerage | +1.0% | All cross-border corridors | Short term (≤ 2 years) |

| Stricter cold-chain pharma rules lifting temperature-controlled volumes | +0.8% | Ontario and Quebec pharma hubs | Long term (≥ 4 years) |

| Source: ���������� | |||

Automotive-Production Rebound Boosting Inbound Parts Flows

Ontario’s assembly plants have restored two-shift operations and are adding battery-module lines that rely on just-in-time parts inflows from the United States suppliers. Brokers coordinate multi-origin consolidations; schedule synchronized deliveries and execute expedited customs entries to prevent costly line stoppages. Expanded zero-emission vehicle incentives heighten this requirement by raising part complexity and shipment frequency. Established intermediaries that combine carrier density with customs expertise capture premium fees for safeguarding on-time performance. As production volumes normalize over the next two years, these value-added coordination services remain integral to automotive competitiveness.

National Trade Corridors Fund Upgrades Expanding Freight Capacity

The NTCF, drawing on its total USD 3.4 billion funding envelope, finances critical infrastructure projects, including terminal and rail yard expansions that shorten dwell times at ports and intermodal hubs. Completed works at the Port of Prince Rupert and Winnipeg’s Symington Yard have improved fluidity, enabling brokers to offer tighter service-level agreements. New overpass projects at the Windsor-Detroit and Pacific Highway crossings likewise reduce border wait times, allowing brokers to negotiate faster asset turns with carriers. As more projects finalize through 2028, network resiliency strengthens, supporting stable pricing and encouraging shippers to shift additional freight to broker-managed multimodal routes. Medium-term gains translate directly into sustained growth for the Canada freight brokerage services market.

Cross-Border E-Commerce Returns Surge Fueling Reverse-Logistics Lanes

Return rates for online apparel and electronics average 25%, creating south-to-north backhauls that once moved empty. Brokers skilled in tariff reclamation and duty drawback aggregate fragmented return loads, recovering value for retailers under CUSMA provisions. Consolidation nodes near Toronto and Vancouver are emerging to stage bulk return shipments, lowering per-unit handling costs. As consumers view no-hassle returns as table stakes, retailers contract brokers capable of seamless cross-border loops. Medium-term momentum is expected to keep reverse-logistics brokerage outpacing forward freight expansion.[2]CBSA, “CARM Program Updates,” cbsa-asfc.gc.ca

Retail-Mandated Real-Time Visibility APIs Accelerating Tech Adoption

Since 2025, Walmart Canada and Loblaw have required API connectivity for inbound freight, forcing brokers to integrate telematics, GPS feeds, and predictive ETA engines. Smaller intermediaries lacking capital are partnering with software vendors or accepting acquisition offers from technology-rich peers. Retailers benefit from proactive exception alerts that reduce shelf-out incidents, cementing API compliance as a vendor qualification standard. Over the long term, visibility mandates will widen the performance gap between brokers with scalable digital infrastructure and those relying on manual processes.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent truck overcapacity compressing brokerage spreads | -1.6% | National, sharper in Western Canada | Short term (≤ 2 years) |

| Digital shipper-carrier marketplaces bypassing traditional brokers | -1.3% | High-volume corridors nationwide | Long term (≥ 4 years) |

| Bill C-27 data-privacy compliance inflating operating costs | -0.9% | All provinces handling personal data | Medium term (2-4 years) |

| Port of Vancouver rail congestion heightening service-level risk | -0.7% | British Columbia, spillover to Alberta | Short term (≤ 2 years) |

| Source: ���������� | |||

Persistent Truck Overcapacity Compressing Brokerage Spreads

Fleet expansions launched during the pandemic outpaced the freight rebound, leaving national capacity utilization near 82%. Carriers chase loads, narrowing the rate margin that brokers traditionally captured between shipper and hauler. Western Canada feels this pressure acutely as resource shipments fluctuate. Brokers counter by bundling customs clearance and mode-optimization services, yet the cost of upgrading technology amid squeezed margins tests financial resilience. Once fleet attrition aligns supply with demand, spread pressure should ease, but short-term profitability remains challenged.

Digital Shipper-Carrier Marketplaces Bypassing Traditional Brokers

Algorithm-driven platforms publish real-time carrier capacity and pricing, letting enterprise shippers contract loads directly. Information asymmetry erodes, and brokers risk disintermediation on commoditized lanes. To defend relevance, incumbents emphasize cross-border complexity, multimodal orchestration, and exception management that digital marketplaces cannot yet automate. Over the long horizon, brokerage margins will depend on specialized services rather than pure load matching, reshaping competitive dynamics across the Canada freight brokerage services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: LTL Consolidation Gains Amid FTL Maturity

Full-truckload maintained 75.37% of the Canada freight brokerage services market share in 2025 on the strength of automotive and manufacturing corridors. Yet less-than-truckload’s 9.45% CAGR through 2031 is outpacing the broader Canada freight brokerage services market size expansion as retailers favor frequent, smaller replenishment loads. Enterprise shippers still rely on FTL brokers to secure backhauls and stabilize capacity, but digital load boards intensify price competition, trimming margins. Consolidators such as RXO are scaling regional cross-dock networks near Toronto and Calgary, combining parcel-sized returns into palletized LTL moves that elevate cube utilization and cut dwell times.

LTL brokerage benefits disproportionately from e-commerce returns flows, where brokers integrate tariff-recovery services with multi-carrier networks. AI-driven routing software clusters pickups geographically, boosting saturation and lowering per-stop cost. FTL incumbents respond by acquiring LTL specialists or embedding consolidation desks within legacy operations. Over the forecast horizon, hybrid models that blend FTL trunk moves with LTL feeder legs maximize network efficiency and preserve share against pure-play digital platforms.[3]Transport Canada, “Transportation in Canada Annual Report,” tc.canada.ca

By Equipment Type: Reefer Demand Outpaces Dry-Van Commoditization

Dry-van trailers held 40.79% of 2025 revenue, but refrigerated van loads are accelerating at a 9.73% CAGR, surpassing the overall Canada freight brokerage services market. Cold-chain compliance for biologics and high-value food elevates average revenue per load, cushioning margins against dry-van rate erosion. Penske Logistics expanded a 75,000-square-foot refrigerated facility outside Toronto in 2025 to stage pharma velocity picks, illustrating infrastructure investment that anchors reefer volume growth.

Dry-van brokerage faces commoditization as digital marketplaces automate matchmaking for standardized freight. Brokers seeking differentiation layer value-added customs and visibility services on top of otherwise routine dry-van moves. The flatbed and tanker segments retain niche importance in energy and construction lanes, but growth remains cyclical and tied to commodity pricing. The long-run trajectory favors brokers that pair validated reefers with data-logging compliance systems in response to tightening Health Canada oversight.

By Haul Length: Urban Last-Mile Surges Despite Long-Haul Dominance

Long-haul shipments exceeding 500 miles controlled 67.92% of the Canada freight brokerage services market size in 2025, underpinning trans-continental trade. However, local hauls under 100 miles are tracking an 11.78% CAGR, well above the systemwide growth driven by same-day delivery commitments in Toronto, Vancouver, and Montreal. Brokers deploy algorithmic route planners that batch store replenishment stops with parcel drop-offs, lifting stop density.

Canada Cartage’s 2024 purchase of a last-mile fleet underscores the pivot toward urban logistics, reflecting retailer pressure for sub-24-hour fulfillment. Regional hauls between 100 and 500 miles link satellite cities and furnish backhaul loads, improving driver home-time metrics that aid recruitment. Margin resilience hinges on mastering urban congestion and tight delivery windows, positioning city-centric brokerage as a high-growth niche within the Canada freight brokerage services market.

By Business Model: Digital Platforms Disrupt Traditional Incumbents

Traditional intermediaries captured 78.30% of 2025 revenue, but digital-first platforms are rapidly scaling at a 27.09% CAGR as algorithmic pricing and instant booking cut administrative overhead. Echo Global Logistics added AI-driven routing modules to defend its share, blending relationship-based carrier procurement with predictive analytics. Asset-based brokers leverage owned tractors and trailers to guarantee surge capacity, commanding premiums from shippers requiring dedicated fleets.

Agent networks broaden legacy firms' geographic reach, but commission splits compress profitability compared with direct digital engagement. Hybrid strategies combining automated rate quoting with human exception handling are emerging as the dominant operating template. Sustained technology spend differentiates scale players from sub-USD 20 million revenue brokers that struggle to fund platform upgrades, accelerating consolidation across the Canada freight brokerage services market.

By End-User Industry: E-Commerce Reshapes Manufacturing Dominance

Manufacturing and automotive freight held a 28.33% share in 2025, yet e-commerce and 3PL fulfillment is powering a 20.15% CAGR through 2031, fueled by direct-to-consumer shipments and inventory decentralization. Retailers outsource fulfillment to specialized 3PLs that demand round-the-clock visibility and flexible capacity. Brokers integrate parcel, LTL, and FTL options into unified dashboards that automate mode selection based on service and cost criteria.

Healthcare and pharmaceuticals carve a premium niche; cold-chain loads incur higher accessorial charges and strict service metrics. Construction and resource industries offer volatile but lucrative project-cargo opportunities, while agriculture drives seasonal demand spikes that reward brokers managing carrier pools with surge flexibility. The diversified mix forces intermediaries to maintain vertical-specific playbooks and regulatory fluency to stay relevant in the evolving Canada freight brokerage services market.

By Customer Size: SMB Growth Challenges Enterprise Concentration

Large shippers above USD 100 million accounted for 68.09% of 2025 loads, leveraging buying power to demand tailored solutions and rate transparency. Small businesses are the fastest-growing cohort at 14.71% CAGR, enabled by self-service portals that reduce administrative friction. Mode Global’s 2024 Vancouver branch launch included a digital onboarding suite allowing shippers to quote, book, and track online without broker intervention.

Tiered service models emerge: white-glove account management for enterprises, web-based spot quoting for SMBs, and subscription bundles for mid-market firms seeking predictable spend. Brokers achieving platform scalability profitability can monetize long-tail SMB volume without eroding enterprise service quality, bolstering total addressable revenue inside the Canada freight brokerage services market.

Geography Analysis

Ontario and Quebec together commanded the majority of brokerage revenue in 2025, anchored by dense automotive, aerospace, and pharmaceutical production corridors. Automotive component flows through Windsor-Detroit crossings, and CBSA’s CARM requirements intensify demand for customs-savvy brokers able to expedite clearance on time-critical parts. Quebec’s pharmaceutical clusters around Montreal require temperature-controlled capacity, strengthening the refrigerated brokerage sub-segment. Toronto-Montreal’s multimodal corridor remains the country’s highest-velocity lane, and real-time visibility mandates from national retailers are first implemented here, setting service benchmarks for other regions.

British Columbia shows the fastest growth pace to 2031 as Pacific trade rebounds and NTCF-funded port expansions at Prince Rupert unlock incremental capacity. Brokers leverage shorter vessel transit times to Asian markets and position differential services such as transloading and cross-docking near Vancouver. Nonetheless, intermittent rail congestion at the Port of Vancouver injects volatility, prompting some shippers to divert to ports in the United States Pacific Northwest. Alberta’s energy-driven tanker and flatbed volumes cycle with commodity pricing, but upcoming carbon-capture projects promise new demand for specialized equipment, supporting brokerage diversification beyond crude and condensate moves.

Atlantic Canada contributes a modest but rising share as seafood exports and forestry products tap expanding the United States demand. Limited carrier density in the Maritimes elevates brokerage importance for securing consistent outbound capacity. Seasonal peaks linked to lobster and snow-crab harvests necessitate rapid brokerage intervention to avoid spoilage. Improved highway links and harmonized interprovincial weight allowances under Transport Canada oversight lower line-haul costs, making the region incrementally more attractive for distribution center siting.[4]Canada Border Services Agency, “CBSA Assessment and Revenue Management (CARM),” cbsa-asfc.gc.ca

The freight brokerage services market is analyzed by ���������� across multiple other geographies, with in-depth regional assessments available for North America and Europe. This is complemented by country-specific insights for Mexico, Brazil, Spain, Spain, Netherlands, Poland, and Saudi Arabia, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Canada’s freight brokerage arena is moderately fragmented, with the top five firms estimated to hold just under 40% of national revenue. Multinationals such as C.H. Robinson, RXO, and DSV differentiate through proprietary platforms that integrate customs modules, predictive ETAs, and carrier scorecards, enabling them to bid on complex, cross-border lanes. Regional specialists concentrate on niche verticals: SPI Logistics emphasizes reverse-logistics for e-commerce returns, while Bison Transport leverages in-house reefer assets to win pharmaceutical contracts.

Acquisitions are the primary path to scale. XPO’s 2024 purchase of an Ontario-Quebec LTL network added 18 terminals, immediately expanding cross-border lane density and lowering empty miles. DSV’s acquisition of a Toronto customs brokerage bolsters CARM-compliant capabilities, providing a regulatory moat against smaller rivals. Private-equity interest is accelerating; platform roll-up strategies focus on digitizing legacy brokers to unlock margin via automation.

Technology remains the defining competitive lever. Echo Global Logistics and Hub Group each invested in AI-based load-pricing engines that learn from carrier acceptance patterns, raising tender success rates. Blockchain pilots, such as Bison Transport’s pharma chain-of-custody ledger, target high-value verticals where immutable temperature data justifies higher freight spend. Firms unable to fund digital transformation are opting for agency affiliations or outright sale, consolidating market power in tech-forward brokers and intensifying competition for carrier capacity within the Canada freight brokerage services market.

Canada Freight Brokerage Services Industry Leaders

C.H. Robinson Worldwide

Total Quality Logistics (TQL)

RXO

J.B. Hunt ICS

Canada Cartage

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: STG announced the acquisition of freight management software provider Carrier Logistics Inc. to accelerate its AI-driven innovation roadmap for LTL and last-mile carriers.

- January 2026: Freight Technologies initiated its transition to an AI-native software provider with the launch of Zayren Pro to automate cross-border carrier matching.

- November 2025: UPS finalized its acquisition of the Canadian third-party logistics provider Andlauer Healthcare Group (AHG) to capture a larger share of the specialized healthcare transportation sector.

- May 2025: SGL Group successfully completed the acquisition of Canadian freight forwarder ITN Logistics Group to rapidly expand its global logistics and transport capacity.

Canada Freight Brokerage Services Market Report Scope

| Full-Truckload (FTL) |

| Less-than-Truckload (LTL) |

| Others |

| Dry Van |

| Refrigerated Van |

| Flatbed / Step-Deck |

| Tanker (Bulk Liquid & Chemical) |

| Others |

| Long-Haul (More than 500 miles) |

| Regional (100-500 miles) |

| Local (Less than 100 miles) |

| Traditional Freight Brokerage |

| Asset-Based Freight Brokerage |

| Agent Model Freight Brokerage |

| Digital Freight Brokerage |

| Manufacturing & Automotive |

| Construction & Infrastructure Projects |

| Oil, Gas, Mining & Chemicals |

| Agriculture & Food / Beverage |

| Retail, FMCG & Wholesale Distribution |

| Healthcare & Pharmaceuticals |

| E-commerce & 3PL Fulfilment |

| Other End-User Industry |

| Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10–100 M) |

| Small Businesses (Less than USD 10 M) |

| By Service | Full-Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| Others | |

| By Equipment / Trailer Type | Dry Van |

| Refrigerated Van | |

| Flatbed / Step-Deck | |

| Tanker (Bulk Liquid & Chemical) | |

| Others | |

| By Haul Length | Long-Haul (More than 500 miles) |

| Regional (100-500 miles) | |

| Local (Less than 100 miles) | |

| By Business Model | Traditional Freight Brokerage |

| Asset-Based Freight Brokerage | |

| Agent Model Freight Brokerage | |

| Digital Freight Brokerage | |

| By End-User Industry | Manufacturing & Automotive |

| Construction & Infrastructure Projects | |

| Oil, Gas, Mining & Chemicals | |

| Agriculture & Food / Beverage | |

| Retail, FMCG & Wholesale Distribution | |

| Healthcare & Pharmaceuticals | |

| E-commerce & 3PL Fulfilment | |

| Other End-User Industry | |

| By Customer Size | Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10–100 M) | |

| Small Businesses (Less than USD 10 M) |

Key Questions Answered in the Report

What is the projected value of the Canada freight brokerage services market in 2031?

The Canada freight brokerage services market is expected to reach USD 2.49 billion by 2031.

How fast is the refrigerated van segment expected to grow?

Refrigerated van brokerage is projected to expand at a 9.73% CAGR through 2031.

Why are small businesses becoming important customers for brokers?

Digital self-service portals lower onboarding barriers, enabling small shippers to access professional freight services and fueling a 14.71% CAGR in that customer cohort.

Which region is anticipated to post the fastest brokerage growth?

British Columbia is set for the quickest expansion, supported by port upgrades and rising Pacific trade flows.

How is the CBSA CARM program influencing brokerage demand?

CARM’s digital customs requirements compel shippers to hire compliant brokers to manage electronic declarations and mitigate penalties, boosting intermediary demand.

What technology investments are brokers prioritizing?

Leading firms are deploying API-based visibility, AI routing engines, and blockchain tracking, meeting retailer mandates for real-time shipment data.

Page last updated on: