United States Medical Display Monitors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

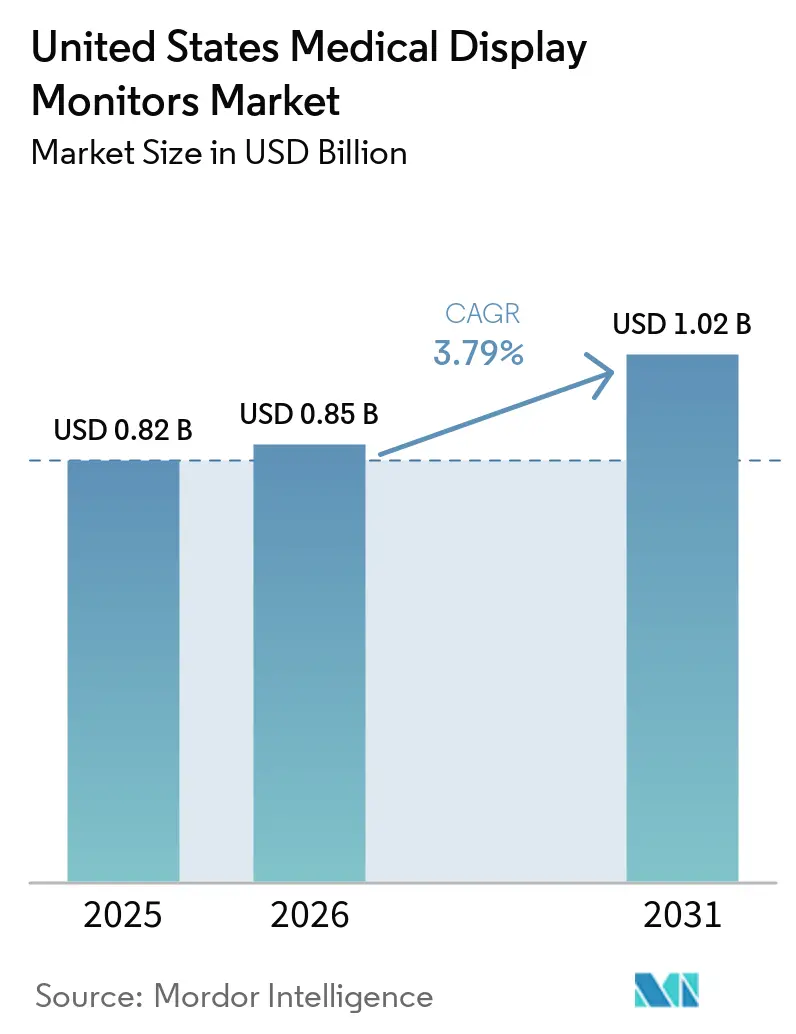

| Base Year Market Size (2025) | USD 0.82 Billion |

| Market Size (2026) | USD 0.85 Billion |

| Market Size (2031) | USD 1.02 Billion |

| Growth Rate (2026 - 2031) | 3.79% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ����������. Reuse requires attribution under CC BY 4.0. | |

United States Medical Display Monitors Market Analysis by ����������

The United States Medical Display Monitors Market size is projected to be USD 0.82 billion in 2025, USD 0.85 billion in 2026, and reach USD 1.02 billion by 2031, growing at a CAGR of 3.79% from 2026 to 2031.

The United States medical display monitors market is moving toward clinically certified hardware because upgrade decisions now depend more on workflow compliance, calibration reliability, and diagnostic accountability than on initial purchase price alone. Procurement demand is being supported by outpatient imaging expansion, reading-room modernization, and a wider upgrade cycle in hybrid operating rooms that are moving to 4K-native visualization platforms. Digital pathology is adding a new layer of demand because FDA-cleared primary diagnosis platforms increasingly tie scanner adoption to approved display configurations, which turns monitor procurement into a compliance requirement instead of a discretionary purchase. Remote viewing tools are expanding clinical access, but they are not removing the need for luminance-calibrated monitors in high-acuity workflows, so the United States medical display monitors market continues to retain a durable hardware base even as software-defined viewing becomes more common. Competitive pressure remains moderate because premium vendors keep an advantage in certification depth, calibration toolchains, and long hospital integration cycles, while smaller OEMs face slower product entry under the 2026 QMSR framework.

Key Report Takeaways

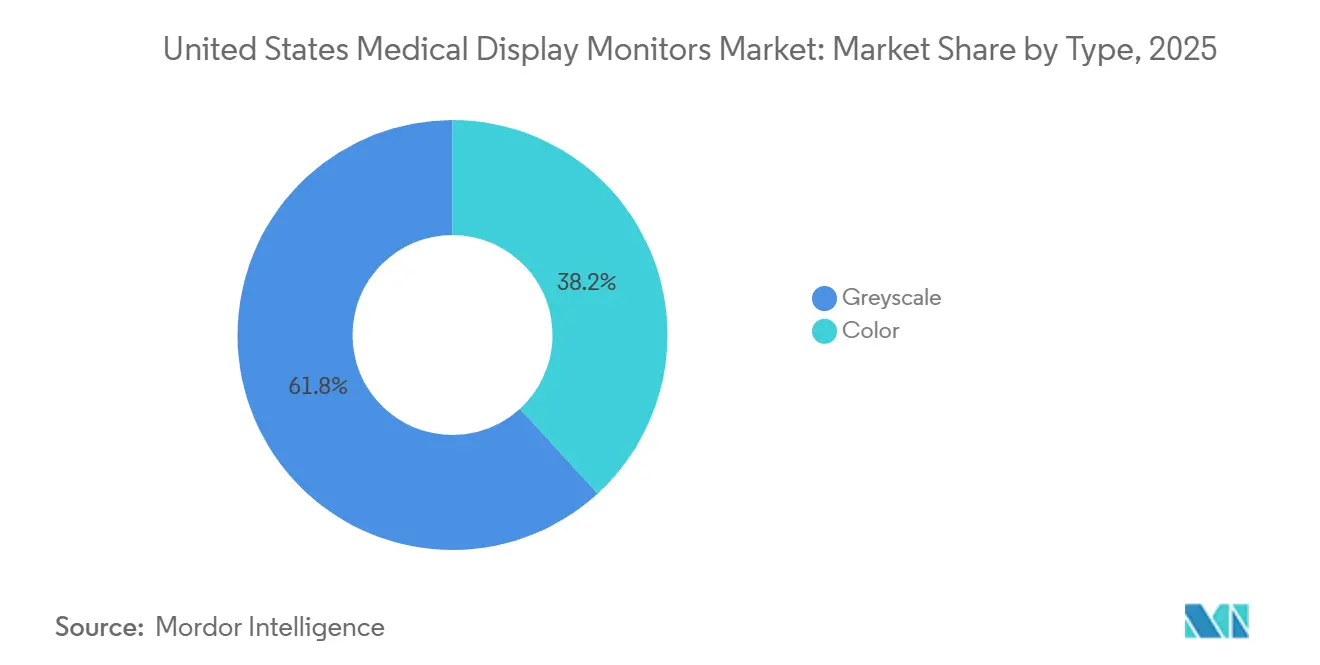

- By type, greyscale held 61.78% of the United States medical display monitors market share in 2025, while color is forecast to expand at a 4.91% CAGR through 2031.

- By resolution, 2.1 MP to 4 MP accounted for 32.16% of the United States medical display monitors market size in 2025, while 4.1 MP to 8 MP is projected to grow at a 4.73% CAGR through 2031.

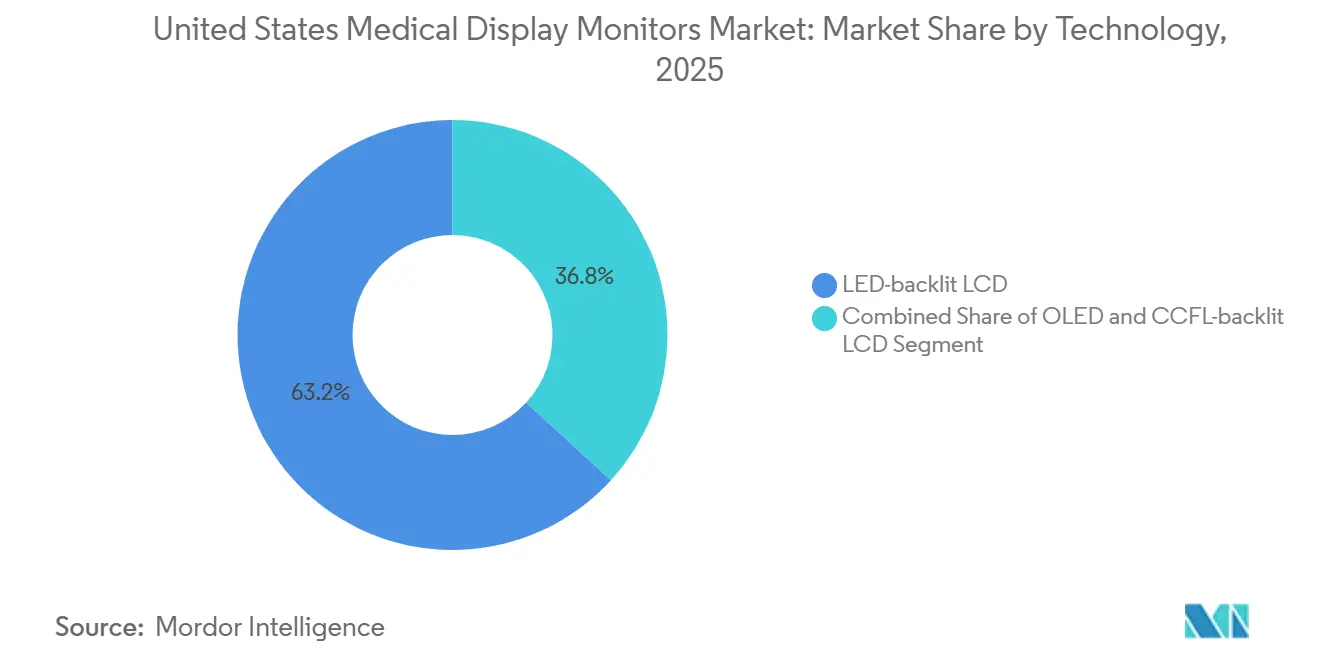

- By technology, LED-backlit LCD led with a 63.23% share in 2025, while CCFL-backlit LCD is expected to record the fastest 5.28% CAGR through 2031.

- By application, surgery and interventional Imaging held 25.74% of the market in 2025, while digital pathology is set to advance at a 5.98% CAGR through 2031.

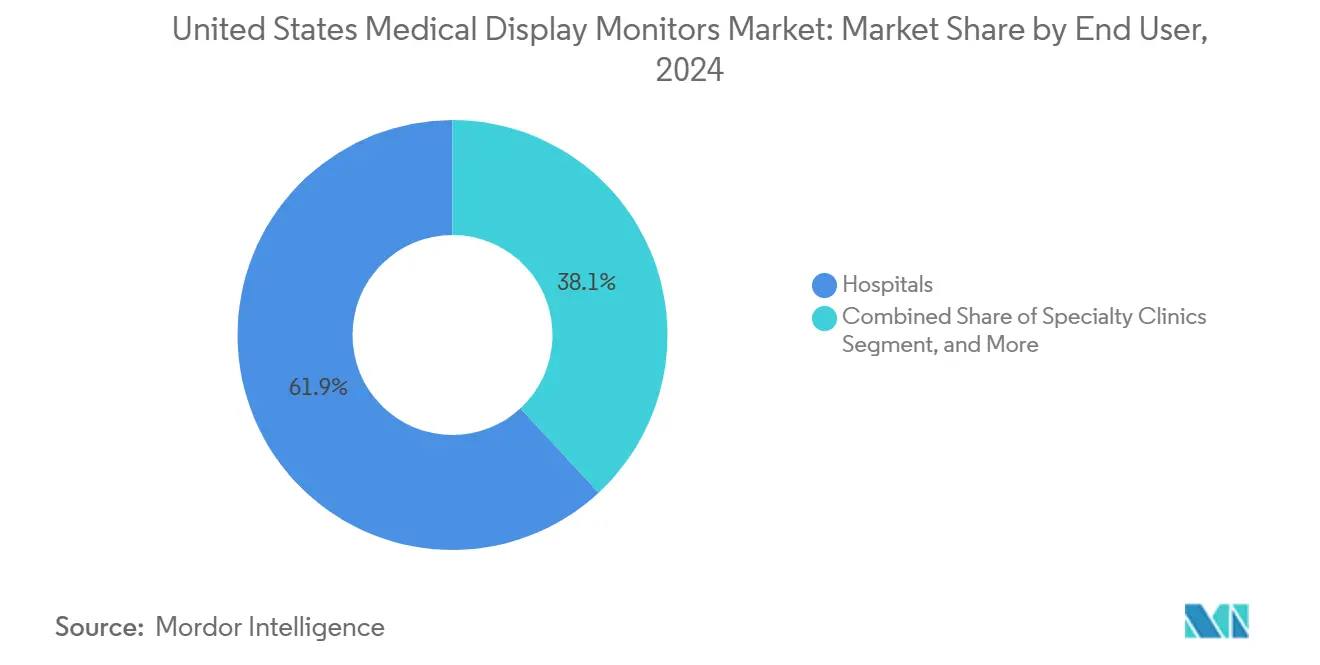

- By end user, hospitals captured 61.86% of the United States medical display monitors market share in 2025, while diagnostic imaging centers and diagnostic laboratories are projected to expand at a 5.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ����������’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Medical Display Monitors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imaging-Center Expansion and Reading-Room Modernization | +0.7% | National, with concentration in Sun Belt, Mid-Atlantic, and urban growth corridors | Short term (≤ 2 years) |

| 4K Minimally Invasive and Hybrid OR Upgrade Cycle | +0.6% | National, early gains in academic medical centers and large integrated health systems | Medium term (2-4 years) |

| Higher Breast Imaging and Oncology Read Volumes | +0.5% | National, with density in high-population states and ACR-accredited screening programs | Short term (≤ 2 years) |

| AI-Enabled Multi-Modality Workflow Complexity Favors Premium Diagnostic Displays | +0.5% | National, with early adoption in hospital-based radiology and academic medical centers | Medium term (2-4 years) |

| FDA-Cleared Digital Pathology Primary Diagnosis Adoption | +0.7% | National, concentrated in large academic hospital networks and commercial reference labs | Medium term (2-4 years) |

| Zero-Footprint Diagnostic Viewing Raising Remote QA Demand | +0.4% | National, with early gains in teleradiology networks and health-system satellite sites | Short term (≤ 2 years) |

| Source: ���������� | |||

Imaging-Center Expansion and Reading-Room Modernization

Outpatient imaging remains one of the clearest near-term demand supports for the United States medical display monitors market. Lumexa Imaging operated more than 190 outpatient centers, completed 4 million procedures in 2025, and added 4 new centers in 2026 through joint ventures with Advocate Health and UPMC while targeting 8 to 10 de novo openings annually.[1]Lumexa Imaging, “Lumexa Imaging Advances Growth Strategy by Adding Four New Imaging Centers,” Lumexa Imaging, lumexaimaging.com Every new center, renovated site, or expanded reading room creates multiple display purchase points across primary diagnostic stations, secondary review screens, and backup work areas. The demand effect is not limited to new buildings because modernization projects also force facilities to reevaluate calibration status, luminance consistency, and monitor age across existing rooms. In the United States medical display monitors market, accreditation-linked procurement behavior matters because facilities that want to maintain high diagnostic standards cannot rely on general commercial screens for every workflow. That pattern supports recurring replacement, recalibration, and service revenue for vendors that can sustain certified QA ecosystems over several years.

4K Minimally Invasive and Hybrid OR Upgrade Cycle

The surgical side of the United States medical display monitors market is entering a more defined 4K and Mini-LED replacement cycle. Sony launched the LMD-32M1MD in January 2025 as the first medical monitor certified to VESA DisplayHDR 1000, and later expanded the lineup in July 2025 with additional 27-inch and 43-inch models for broader procedural use. LG also received FDA 510(k) clearance in September 2025 for the 32HS710S 4K surgical monitor, while EIZO stated that its CuratOR EX3245H Mini-LED model would begin shipping in November 2026 with 1,900 cd/m² peak brightness and a 1,000,000:1 contrast ratio. These launches matter because a large installed base of pre-4K HD displays from 2015 to 2020 is aging out of its preferred service window in operating rooms and ambulatory settings.[2]LG Electronics, “LG Launches 4K Surgical Monitor with Intelligent Features to Optimize Surgical Workflow,” LG Global Business, lg.com Many older systems were purchased for cost efficiency, not for fluorescence guidance, robotic assistance, or sustained high dynamic range performance during long procedures. That gap is creating a replacement wave in the United States medical display monitors market that should stay active as hospitals and ASCs standardize their OR visualization stacks.

FDA-Cleared Digital Pathology Primary Diagnosis Adoption

Digital pathology is becoming one of the strongest structural demand drivers in the United States medical display monitors market. Roche received FDA clearance for the DP 200 in June 2024 and for the higher-volume DP 600 in January 2025, while PathAI received FDA clearance for AISight Dx in June 2025 and Indica Labs received clearance for HALO AP Dx in December 2025.[3]Roche, “Roche Receives FDA Clearance on Its Digital Pathology Solution for Diagnostic Use,” Roche Diagnostics, diagnostics.roche.com The key procurement implication is that approved digital pathology systems are not just scanners and software because display models are often specified in the regulatory package. That creates a compliance-driven pull for certified color monitors in pathology labs that previously relied on optical microscopy and had no comparable display requirement. Labcorp expanded its collaboration with PathAI in February 2026 to deploy AISight Dx across its national network, which indicates that large-scale pathology rollout is now moving from pilot activity to operational implementation. In the United States medical display monitors market, this is an additive demand because many pathologists are entering a digital display procurement cycle for the first time. The result is a new installed base that depends on color accuracy, high pixel density, and repeatable calibration for primary diagnosis.

AI-Enabled Multi-Modality Workflow Complexity Favors Premium Diagnostic Displays

AI integration is raising the performance threshold across the United States medical display monitors market. GE HealthCare received FDA 510(k) clearance in March 2026 for Genesis View, a zero-footprint diagnostic viewer with AI-enabled 2D and 3D visualization that connects directly to Advanced Visualization applications. As more facilities add AI overlays, segmentation masks, automated measurements, and confidence maps to the reading workflow, the display becomes more than a passive screen. Older monitors that remain acceptable for basic greyscale review may not deliver the color consistency or spatial stability needed for AI-assisted interpretation across multiple modalities. A 2025 article in the Journal of Imaging Informatics in Medicine showed that native deep-learning model integration into radiological viewers depends on controlled rendering pipelines, which supports the case for certified display environments rather than ad hoc viewing setups. This matters for the United States medical display monitors market because hospitals are activating AI inside workflows they already operate, which turns existing monitor fleets into potential bottlenecks. Premium diagnostic displays, therefore, gain an advantage as facilities try to align software sophistication with dependable visual output at the workstation level.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Acquisition Cost for Premium Diagnostic and Surgical Displays | -0.6% | National, with greater pressure on rural hospitals and smaller independent imaging centers | Short term (≤ 2 years) |

| Long Replacement Cycles and Lower-Cost Substitute Pressure | -0.5% | National, with higher impact in outpatient and ambulatory settings | Medium term (2-4 years) |

| 2026 QMSR Compliance Burden for Device Makers | -0.3% | National, concentrated among smaller display OEMs and importers without prior ISO 13485 certification | Medium term (2-4 years) |

| Web Viewer Adoption Deferring Some Dedicated Workstation Display Upgrades | -0.4% | National, with early displacement in low-acuity teleradiology and health-system satellite sites | Short term (≤ 2 years) |

| Source: ���������� | |||

High Acquisition Cost for Premium Diagnostic and Surgical Displays

High-end medical displays remain expensive enough to slow unit adoption in parts of the United States medical display monitors market. EIZO launched the RadiForce GX570 in April 2026 as a 5 MP monochrome mammography monitor with a 2,200:1 contrast ratio and an Instant Backlight Booster that reaches 2,500 cd/m², while Barco positioned Coronis OneLook as a 32 MP breast imaging display for full-resolution review. The gap between a certified medical display and a high-performance commercial monitor can reach USD 5,000 to USD 20,000 per unit, which is significant for smaller facilities that need several stations at once. Accreditation standards still create a floor under demand, because luminance verification and DICOM calibration are not optional in many clinically sensitive workflows. Even so, budget pressure is strongest in rural hospitals, independent imaging operators, and lower-volume specialty settings where capital committees review every replacement closely. This keeps procurement disciplined and slows the speed at which the United States medical display monitors market can fully migrate to the highest resolution and brightest premium tiers.

Long Replacement Cycles and Lower-Cost Substitute Pressure

Replacement cycles are long in the United States medical display monitors market because certified displays are built for extended stability and service life. Many reading rooms equipped between 2018 and 2020 with 3 MP to 5 MP DICOM-calibrated screens can remain technically serviceable into 2028 through 2030 if no major workflow change forces replacement. Commercial monitors have also improved, and third-party calibration support allows some secondary review applications to function without a fully certified medical display. Zero-footprint viewing platforms reinforce that pressure because clinicians can access images in more locations without installing a dedicated workstation at every site. That substitution path is most visible in teleradiology and satellite environments, where convenience can outweigh the benefits of a dedicated room in low-acuity tasks. The result is slower unit turnover, which moderates volume growth in the United States medical display monitors market, even while average selling prices remain firm in premium categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Greyscale Holds the Largest Installed Base While Color Expands Faster

Greyscale displays held 61.78% of the United States medical display monitors market share in 2025, which confirms that monochrome visualization still anchors routine radiology and mammography reading volumes. Color displays are projected to record the faster 4.91% CAGR through 2031 as pathology and surgical workflows demand stronger tissue hue fidelity and broader visual context. The United States medical display monitors market still relies on greyscale for high-volume diagnostic work because DICOM GSDF-calibrated monochrome rendering remains the clinical standard for many radiology tasks. That installed base gives greyscale an enduring advantage in replacement demand, even when new use cases are shifting toward color.

Color demand is expanding for clear workflow reasons rather than for cosmetic preference. FDA-cleared pathology systems increasingly reference approved color displays as part of the diagnostic setup, which means monitor selection now sits inside regulated deployment planning instead of general IT sourcing. Surgical visualization is also inherently color dependent because fluorescence guidance, perfusion imaging, and robotic procedures depend on stable rendering during long cases. At the same time, the United States medical display monitors industry is still investing in greyscale product performance, which is visible in EIZO’s April 2026 launch of the RadiForce GX570 for mammography use. The type landscape is therefore splitting into 2 durable demand pools, one centered on radiology continuity and another centered on expanding color-critical workflows. That balance keeps greyscale large while allowing color to gain share over the forecast period.

By Resolution: Mid-Range Volume Leads While Higher Resolution Gains Strategic Importance

The 2.1 MP to 4 MP band accounted for 32.16% of the United States medical display monitors market size in 2025, which reflects the deep installed base of 3 MP-class workstations used across general imaging and review environments. This band remains the practical center of the market because it covers many diagnostic tasks while staying more accessible to facilities with tighter capital budgets. The United States medical display monitors market continues to favor this range for broad deployment because it offers a workable balance between clinical utility and procurement cost. That is why community hospitals and many outpatient sites still fall within this mid-range tier.

The 4.1 MP to 8 MP band is forecast to grow at a 4.73% CAGR through 2031 as mammography and whole-slide imaging create stronger demand for sustained high-resolution rendering. The April 2024 USPSTF breast cancer screening recommendation lowered the starting age for routine screening to 40, which expands the long-term screening base and supports continued equipment demand in accredited breast imaging settings. At the top end, Barco’s Coronis OneLook brings 32 MP capability to breast imaging review, showing how premium resolution is being used to improve throughput in high-volume programs. The United States medical display monitors industry is therefore seeing a reshaping effect rather than a full migration, because mid-range remains dominant while high-resolution demand expands in clinically specific settings. Segments above 8 MP stay niche, but their relevance is rising in breast imaging, advanced surgical applications, and specialized academic environments where panning reduction and full-field review matter.

By Technology: LED-Backlit LCD Leads the Core Market While Legacy Platforms Still Find Use

LED-backlit LCD held 63.23% share in 2025, which makes it the dominant technology platform in the United States medical display monitors market. Its lead comes from long vendor support history, familiar DICOM calibration workflows, and continued performance gains across diagnostic and surgical products. The technology also benefits from broad clinician acceptance because it is already embedded across reading rooms, OR displays, and review stations. That combination keeps LED-backlit LCD at the center of both new installations and standard replacement cycles.

Product launches continue to reinforce that position. Sony expanded its HDR-certified surgical monitor lineup in July 2025, and EIZO stated that its first Mini-LED surgical monitor would begin shipping in November 2026, showing that premium performance is still being pushed within LED-derived architectures. OLED remains present at the surgical premium end, but adoption is limited by panel cost and long-use concerns in high-brightness environments. The unexpected pattern is that CCFL-backlit LCD is projected to grow fastest at 5.28% CAGR through 2031 because refurbished certified units still appeal to smaller providers trying to extend reading-room capability at lower cost. In the United States medical display monitors market, this does not signal a return to legacy technology leadership. It shows that a meaningful installed base still values compliant, lower-cost refurbishment in community, rural, and safety-net settings where capital efficiency matters.

By Application: Surgical Visualization Leads Current Revenue While Digital Pathology Grows Fastest

Surgery and Interventional Imaging held 25.74% of the United States medical display monitors market size in 2025, making it the largest application segment. This position reflects the fact that display hardware is deeply embedded inside OR integration platforms, camera towers, endoscopy stacks, and visualization systems. Hospitals and ASCs cannot easily separate the display decision from the larger procedural platform decision in these settings. That gives surgical visualization a strong current revenue base inside the United States medical display monitors market.

Digital Pathology is forecast to expand at a 5.98% CAGR through 2031, which makes it the fastest-growing application area. The main driver is regulatory and operational at the same time, because FDA-cleared pathology platforms identify approved digital workflows and display dependencies that facilities must follow for primary diagnosis. KARL STORZ and Smith+Nephew also announced a strategic relationship in February 2026 that combined visualization, 3D imaging, fluorescence, and OR integration capabilities for hospital and ASC settings, which shows how display demand is increasingly tied to broader system packages. General radiology and mammography remain steady base applications, while clinical review and telemedicine show a mixed pattern of broader access and stronger software substitution. The United States medical display monitors industry is therefore being shaped by both embedded procedural hardware demand and new pathology deployment, not by one application alone.

By End User: Hospitals Remain the Core Buyers While Outpatient Channels Expand Faster

Hospitals held 61.86% of the United States medical display monitors market share in 2025, which confirms that large health systems remain the main source of capital demand for diagnostic and procedural display infrastructure. Their scale matters because they usually procure through structured contracts, service agreements, and group purchasing channels that favor vendors with strong integration support. The United States medical display monitors market therefore remains anchored by hospital replacement cycles, enterprise standards, and multi-site workflow consistency. This gives established suppliers a clear advantage in large competitive bids.

Diagnostic Imaging Centers and Diagnostic Laboratories are projected to grow at a 5.47% CAGR through 2031, making them the fastest-growing end-user group. Lumexa Imaging’s 2025 procedure volume and ongoing center expansion show why outpatient operators are becoming a more meaningful procurement engine for reading-room displays and clinical review stations. Specialty clinics also add demand in oncology and breast health, while ASCs are increasingly relevant for surgical monitor placement as procedures continue to move outside hospital ORs. Even with this outpatient shift, accreditation-linked calibration requirements limit how far facilities can defer certified display investment in clinically sensitive use cases. That is why hospitals remain the base of the market while outpatient channels supply a larger share of incremental growth.

Geography Analysis

The United States holds the lead because it combines outpatient imaging expansion, structured accreditation requirements, and faster uptake of AI-assisted clinical workflows in both hospital and ambulatory settings. Lumexa Imaging’s 190-plus center network and its continued 2026 expansion activity show how distributed imaging capacity supports new reading-room and review-screen demand across multiple states. Procurement in these countries often favors established vendors that can show strong service support, certified quality systems, and integration reliability across large institutional accounts. This creates a disciplined buying environment that resembles the higher end of the United States medical display monitors market, even if budget structures differ by country. Together, these regions shape supplier strategy around export pipelines, feature localization, and service support that also influence product positioning in the United States medical display monitors market.

Competitive Landscape

The United States medical display monitors market is moderately fragmented, with a concentrated premium tier and a broader field of specialized mid-market suppliers. Barco NV, EIZO Corporation, Sony Group Corporation, and Stryker Corporation remain the most visible names across premium diagnostic and surgical environments. Their position comes less from price competition and more from certification history, workflow fit, calibration support, and long replacement cycles inside hospital systems. That keeps competition active, but it also slows rapid displacement by smaller entrants.

Barco continues to stand out in premium diagnostic imaging. Its Coronis OneLook launched in January 2026 as a 32 MP breast imaging display aimed at full-resolution review, and the company also supported the clinically cleared Eonis Vision glasses-free 3D platform through its partnership with Avatar Medical in April 2026. EIZO is active across diagnostic and surgical tiers, with the RadiForce GX570 strengthening mammography and the CuratOR EX3245H marking its first Mini-LED surgical platform. Sony also set a clear benchmark in January 2025 when it introduced the first medical monitor with VESA DisplayHDR 1000 certification, which gave it a strong quality signal in the surgical visualization segment. These product moves show that premium competition in the United States medical display monitors market is being defined by performance ceilings and clinical fit rather than rapid commoditization.

The surgical side is increasingly shaped by ecosystem bundling. KARL STORZ and Smith+Nephew announced a strategic relationship in February 2026 to combine advanced visualization, 3D imaging, NIR and ICG fluorescence, and OR integration with sports medicine solutions across hospitals and ASCs. That kind of partnership reduces the importance of standalone display selection in some procedural settings because the screen is sold as part of a broader platform. Mid-tier specialists such as FSN Medical Technologies and Double Black Imaging still matter because they compete on cost, refurbishment depth, and practical integration support for community hospitals and outpatient centers. The result is a market where premium leaders dominate the highest-acuity niches, but smaller specialists still retain room in cost-sensitive accounts. This balance is why the United States medical display monitors market does not show the profile of a highly consolidated category, even though brand credibility remains very important.

United States Medical Display Monitors Industry Leaders

HP Development Company, L.P

Steris

LG Electronics Inc.

Stryker Corporation

Barco NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Lumexa Imaging added 4 new outpatient imaging centers across Spartanburg, SC, Concord, NC, Wexford, PA, and Niceville, FL, bringing its nationwide total to 190+ centers after conducting 4 million procedures system-wide in 2025. Two locations were executed through joint ventures with Advocate Health and UPMC, and the expansion directly increases reading-room display procurement demand across Sun Belt and Mid-Atlantic markets.

- April 2026: Avatar Medical received FDA 510(k) clearance for Avatar Medical Vision for use with Barco's Eonis glasses-free 3D display, creating the first clinically cleared glasses-free 3D medical imaging platform. The Barco and Avatar Medical Eonis Vision bundle establishes a new premium display category for specialist clinical consultations and patient communication in the United States market.

- March 2026: GE HealthCare received FDA 510(k) clearance for View, the zero-footprint diagnostic viewer within the Genesis Radiology Workspace. Designed for anywhere access with AI-enabled 2D and 3D visualization and direct Advanced Visualization application connectivity, View expands diagnostic-quality remote review and increases the need for QA-compliant viewing environments at remote radiologist sites.

- February 2026: Labcorp expanded its collaboration with PathAI to deploy AISight Dx, an FDA-cleared digital pathology platform, across its national network of anatomic pathology labs and hospital collaborations. This nationwide rollout drives direct demand for certified color medical display monitors in pathology labs shifting from optical microscopy to whole-slide digital imaging.

United States Medical Display Monitors Market Report Scope

As per the scope, medical display monitors are specialized monitors tailored to meet the rigorous demands of medical imaging. Each display is crafted for a distinct specialty, including radiology, breast imaging, surgery, digital pathology, and dentistry.

The United States Medical Display Monitors Market Report is Segmented by Type (Greyscale, Color), Resolution (Up to 2 MP, 2.1 MP to 4 MP, 4.1 MP to 8 MP, Above 8 MP), Technology (LED-backlit LCD, OLED, CCFL-backlit LCD), Application (General Radiology and Diagnostic Imaging, Mammography, Surgery and Interventional Imaging, Digital Pathology, Dentistry, Clinical Review, Education, and Telemedicine), End User (Hospitals, Diagnostic Imaging Centers and Diagnostic Laboratories, Specialty Clinics, Ambulatory Surgical Centers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Greyscale |

| Color |

| Up to 2 MP |

| 2.1 MP to 4 MP |

| 4.1 MP to 8 MP |

| Above 8 MP |

| LED-backlit LCD |

| OLED |

| CCFL-backlit LCD |

| General Radiology and Diagnostic Imaging |

| Mammography |

| Surgery and Interventional Imaging |

| Digital Pathology |

| Dentistry |

| Clinical Review, Education, and Telemedicine |

| Hospitals |

| Diagnostic Imaging Centers and Diagnostic Laboratories |

| Specialty Clinics |

| Ambulatory Surgical Centers |

| By Type | Greyscale |

| Color | |

| By Resolution | Up to 2 MP |

| 2.1 MP to 4 MP | |

| 4.1 MP to 8 MP | |

| Above 8 MP | |

| By Technology | LED-backlit LCD |

| OLED | |

| CCFL-backlit LCD | |

| By Application | General Radiology and Diagnostic Imaging |

| Mammography | |

| Surgery and Interventional Imaging | |

| Digital Pathology | |

| Dentistry | |

| Clinical Review, Education, and Telemedicine | |

| By End User | Hospitals |

| Diagnostic Imaging Centers and Diagnostic Laboratories | |

| Specialty Clinics | |

| Ambulatory Surgical Centers |

Key Questions Answered in the Report

What is the 2031 outlook for medical display monitors in the United States?

The market is forecast to reach USD 1.02 billion by 2031 from USD 0.85 billion in 2026, rising at a 3.79% CAGR over 2026-2031.

Why do greyscale monitors still lead clinical use in the United States?

Greyscale displays held 61.78% share in 2025 because radiology, mammography, and other high-volume diagnostic workflows still depend on DICOM-optimized monochrome rendering.

Which product segment is growing the fastest?

Color displays are growing fastest at a 4.91% CAGR through 2031 as digital pathology and surgical visualization require stronger color fidelity.

Which resolution band is seeing the strongest growth?

The 4.1 MP to 8 MP segment is projected to grow at a 4.73% CAGR through 2031, supported by mammography and whole-slide imaging requirements.

What is driving demand from pathology labs?

FDA-cleared primary diagnosis platforms from Roche, PathAI, and Indica Labs are pushing pathology labs toward certified color displays tied to regulated digital workflows.

Page last updated on: