Beef Cattle Feed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

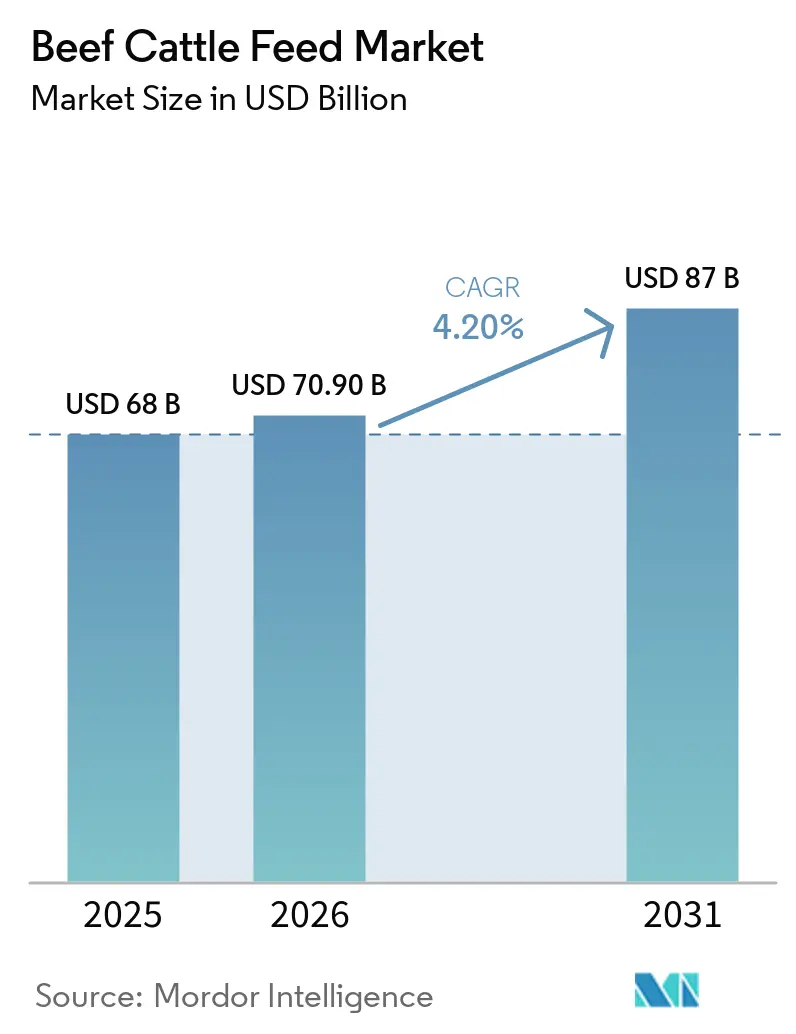

| Market Size (2026) | USD 70.90 Billion |

| Market Size (2031) | USD 87 Billion |

| Growth Rate (2026 - 2031) | 4.20% CAGR |

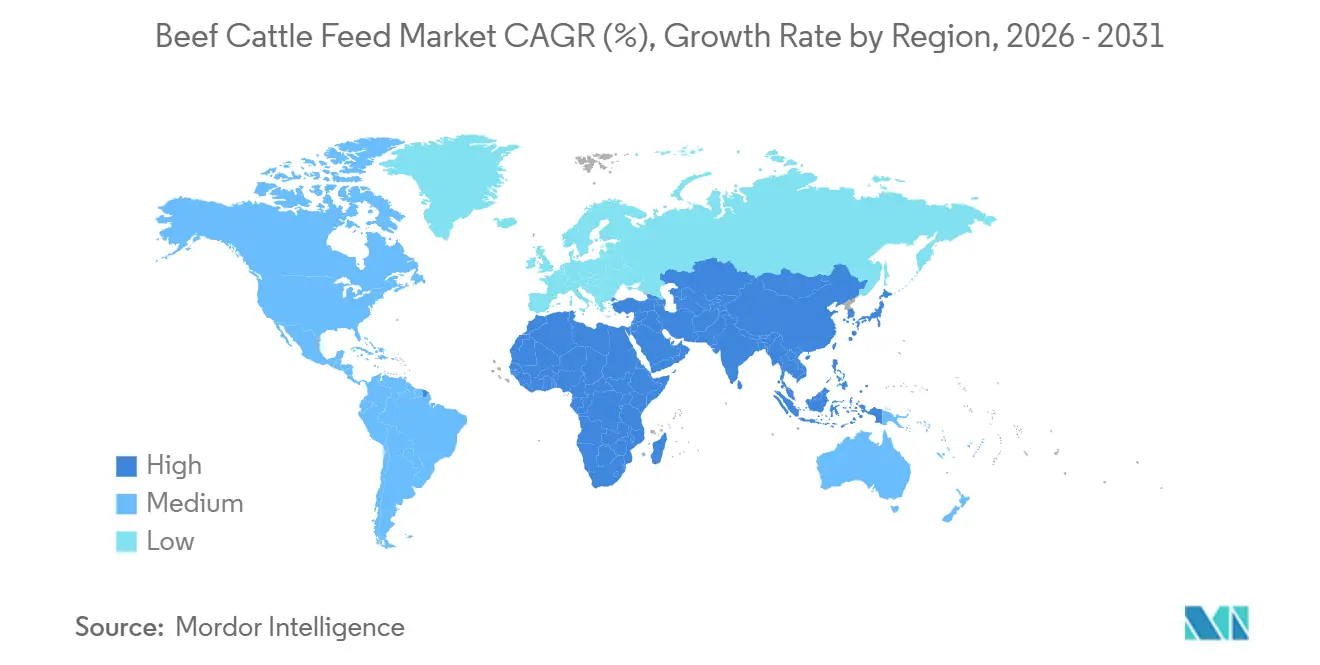

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

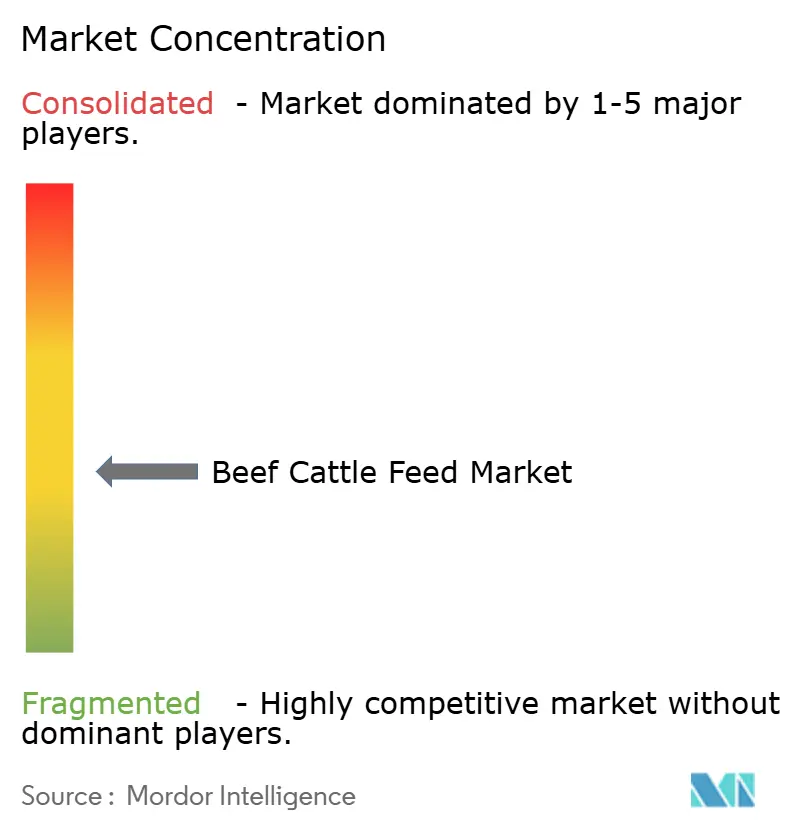

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ����������. Reuse requires attribution under CC BY 4.0. | |

Beef Cattle Feed Market Analysis by ����������

The beef cattle feed market size is projected to increase from USD 68.0 billion in 2025 to USD 70.9 billion in 2026 and is forecast to reach USD 87.0 billion by 2031 at 4.2% CAGR over the forecast period (2026-2031). Growth in the beef cattle feed market is being supported by stronger commercial feedlot intensity and rising per-capita beef consumption in emerging economies. Global beef feed tonnage increased by 0.5% in 2025 to 134.2 million metric tons, which showed that heavier finishing weights and higher feedlot throughput mattered more than herd expansion in the current cycle[1]Source: Alltech, “Agri-Food Outlook 2026,” Alltech, assets.ctfassets.net. OECD-FAO expects total global meat consumption to rise by 12% by 2033, and Asia-Pacific per-capita beef intake is set to increase by 0.5 kg per year, which supports higher-energy finishing rations and wider use of formulated feed solutions in the beef cattle feed market. Feed companies are responding by expanding premix capacity, using precision ration tools, and building stronger compliance-based product portfolios rather than competing only on commodity volume in the beef cattle feed market. Opportunity remains strongest where industrial finishing systems are scaling and where sustainability and traceability requirements are pushing buyers toward functional ingredients, specialty premixes, and science-backed formulations in the beef cattle feed market.

Key Report Takeaways

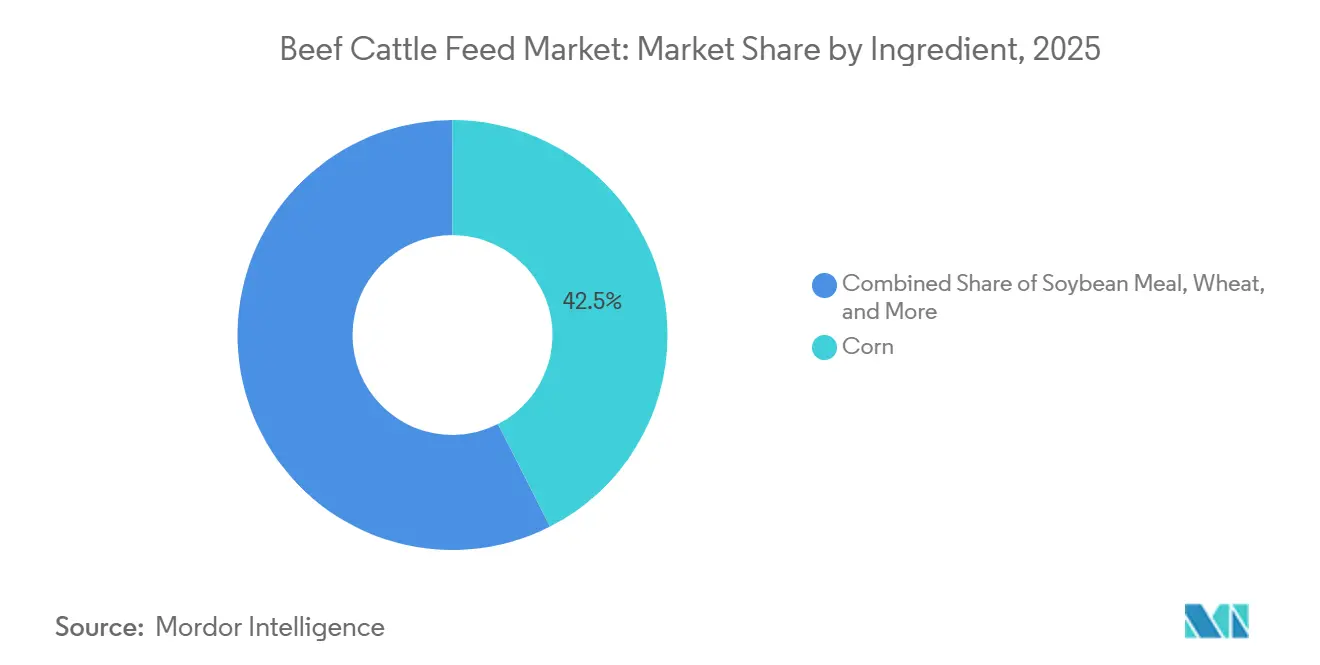

- By ingredient, corn led with 42.5% revenue share in 2025, while insect protein meal is forecast to expand at 14.2% CAGR through 2031.

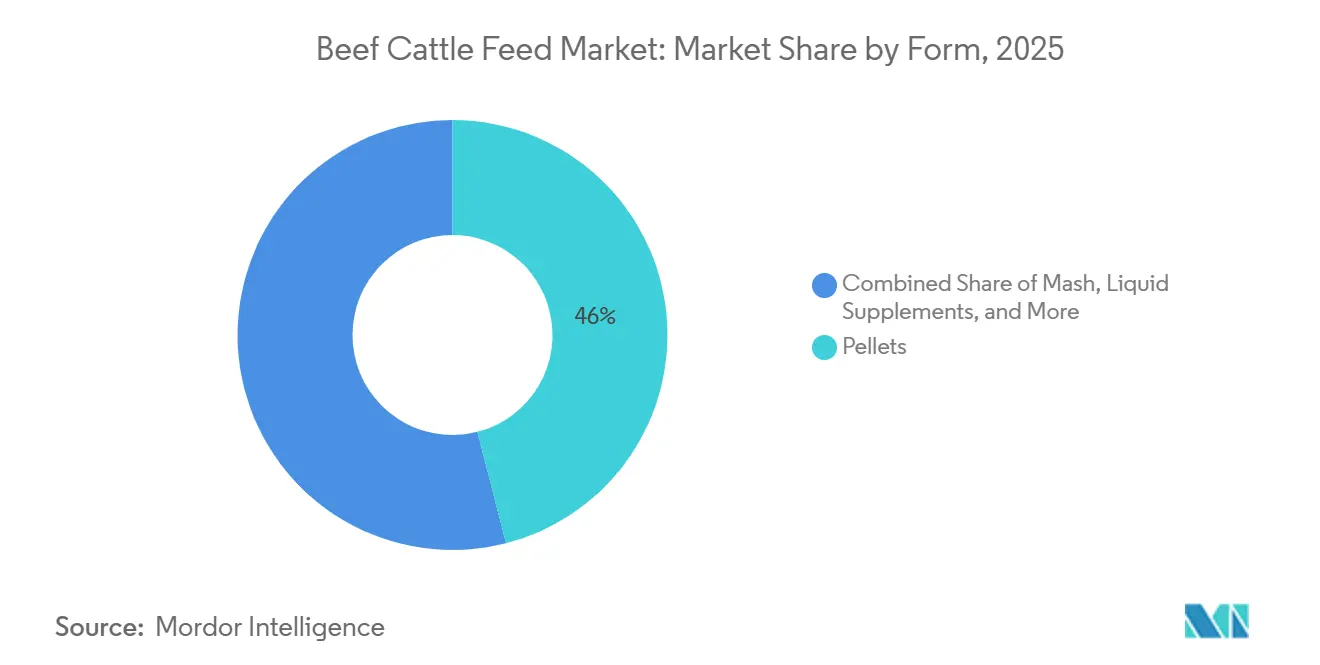

- By form, pellets accounted for 46.0% of the beef cattle feed market size in 2025, while liquid supplements are advancing at 8.7% CAGR through 2031.

- By feed type, complete feed held 52.0% revenue share in 2025, while premixes and specialty additives are projected to grow at 6.8% CAGR through 2031.

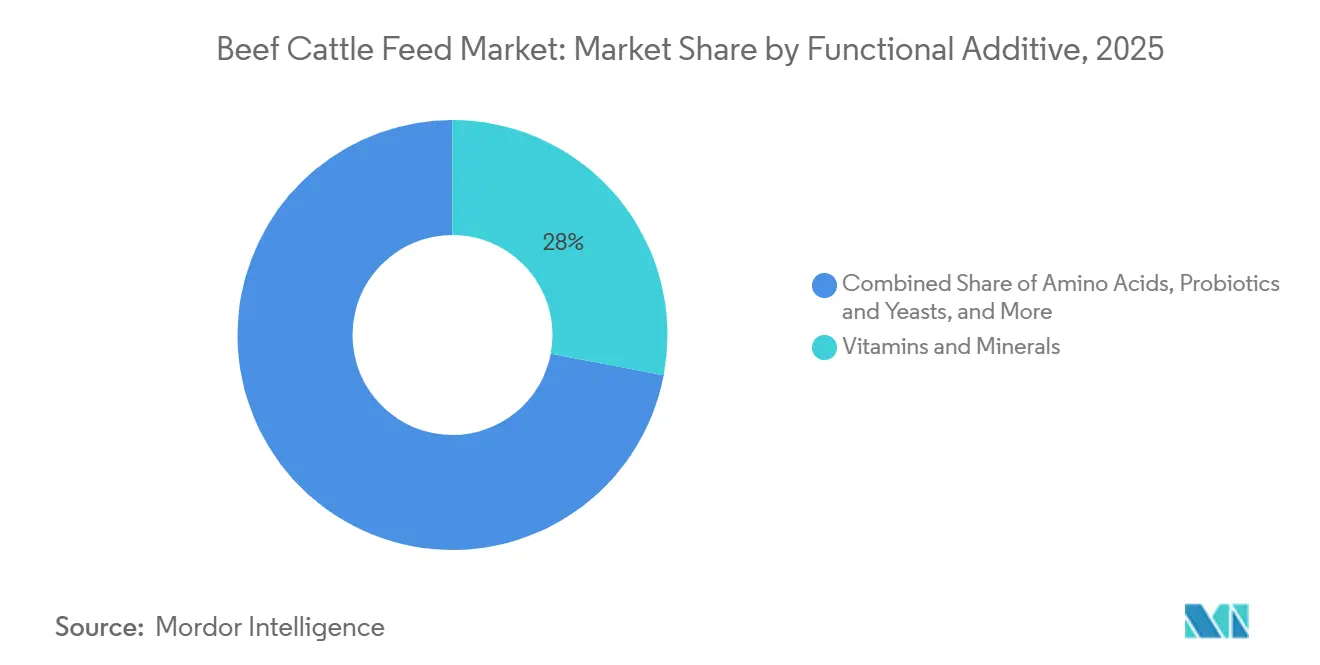

- By functional additive, vitamins and minerals captured 28.0% revenue share in 2025, while rumen-protected amino acids are forecast to expand at 9.8% CAGR through 2031.

- By geography, North America held 33% of the beef cattle feed market share in 2025, while the Asia-Pacific is forecast to grow at 5.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ����������’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Beef Cattle Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Protein-dense beef demand supporting commercial feed adoption | +1.0% | Global | Short term (≤ 2 years) |

| Antibiotic-free beef premiums accelerating specialty additive demand | +0.8% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Methane-reduction compliance increasing demand for functional feed solutions | +0.6% | Europe core, with spillover to Australia and Canada | Medium term (2-4 years) |

| Precision ration formulation improving feed efficiency and weight gain | +0.7% | North America, Australia, and Brazil | Medium term (2-4 years) |

| Carbon-credit monetization encouraging low-emission feed programs | +0.4% | North America, Australia, and Brazil | Long term (≥ 4 years) |

| Hindgut and rumen stability needs in high-grain finishing systems | +0.5% | United States, Brazil, Australia, Mexico, and Argentina | Medium term (2-4 years) |

| Source: ���������� | |||

Protein-Dense Beef Demand Supporting Commercial Feed Adoption

Global demand for beef protein continues to drive volume growth in the beef cattle feed market. According to OECD-FAO projections, global meat consumption is estimated to increase by 12% by 2033, with South and Southeast Asia as key demand centers driven by rising incomes and changing dietary preferences[2]Source: OECD and FAO, “Agricultural Outlook 2024-2033,” OECD, oecd.org . This growing demand is not only leading to an increase in animal numbers in certain countries but is also encouraging producers to aim for heavier slaughter weights and more consistent carcass performance. As a result, higher-energy rations are becoming increasingly important, boosting the use of corn, oilseed cakes, and performance supplements over traditional low-input forage systems in the beef cattle feed market. This trend is evident even in regions where cattle inventories are under pressure, as intensified finishing practices have compensated for herd reductions. Alltech, Inc. reported that global beef feed tonnage increased by 0.5% from 2024 to 2025, despite declining cattle inventories in North America and Europe. This pattern highlights the resilience of commercial feed adoption in the beef cattle feed market, as production gains are increasingly driven by finishing efficiency and ration quality rather than herd expansion alone.

Antibiotic-Free Beef Premiums Accelerating Specialty Additive Demand

Antibiotic-free and no-antibiotics-ever programs are becoming standard across major retail and foodservice supply chains in North America, Europe, and Asia-Pacific, especially Japan. This has increased demand for probiotics, direct-fed microbials, yeast cultures, organic acids, and phytogenics in the beef cattle feed market that support gut health and performance without medicated growth promoters. Buyers also prioritize traceability, ingredient identity, and formulation consistency, increasing preference for specialty inputs over generic products. As a result, suppliers offering proven efficacy and strong documentation are gaining importance in the beef cattle feed market. For example, in May 2024, Alltech, Inc. began North American distribution of Agolin Ruminant, a Carbon Trust-certified feed additive for methane reduction. The product supported cleaner-label livestock programs and strengthened verified sustainability claims for producers and buyers. As premium beef channels expand, documented specialty nutrition is anticipated to gain further importance over generic additives with limited traceability.

Methane-Reduction Compliance Increasing Demand for Functional Feed Solutions

Emission reporting rules are moving from voluntary disclosure to formal buyer and regulatory requirements in the beef cattle feed market. Under the European Union’s Corporate Sustainability Reporting Directive, Scope 3 emissions from livestock became a legal reporting requirement in 2026, which is changing procurement standards for feed and additive suppliers. Feed buyers are therefore giving greater weight to proven methane-reducing inputs such as 3-nitrooxypropanol, tannins, and phytogenic blends, as well as to suppliers that can document life-cycle impacts. Nutreco also received a Dutch grant in February 2025 for a project aimed at reducing ammonia emissions by 10% to 20% per beef cattle without lowering meat output. These developments show that compliance spending is now supporting new product development and wider commercial use of functional formulations in the beef cattle feed market

Precision Ration Formulation Improving Feed Efficiency and Weight Gain

Precision nutrition tools are making the beef cattle feed market more performance-driven and less dependent on broad formulation averages. Near-infrared scanning connected to cloud-based ration software is helping nutritionists measure actual feed quality in real time, rather than relying solely on periodic lab checks. Trouw Nutrition expanded this approach further in May 2026 through a partnership with QuantumBasel to leverage a proprietary database covering more than 600 studies in animal nutrition. This improves control over raw material variation, reduces overuse of expensive minerals and amino acids, and supports more stable performance in commercial feedlot systems. Cargill’s June 2025 investment in its Fort Morgan beef plant included the CarVe computer vision system for real-time yield measurement, which links downstream carcass data with upstream nutrition decisions more directly than before. Together, these systems are strengthening the value proposition for data-led feeding programs in the beef cattle feed market by improving both cost control and biological performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corn and Soybean Meal Price Volatility Pressuring Feed Margins | -1.2% | Global | Short term (≤ 2 years) |

| Additive Approval and Antibiotic-Use Restrictions Slowing Product Rollouts | -0.6% | Europe, North America, and Asia-Pacific | Medium term (2-4 years) |

| Cultivated-Meat Investment Affecting Long-Term Beef Demand Planning | -0.3% | North America, Europe, and Singapore | Long term (≥ 4 years) |

| Storage and Handling Variability Reducing Specialty Feed Performance | -0.4% | Middle East and Africa, Asia-Pacific core, and South America | Medium term (2-4 years) |

| Source: ���������� | |||

Corn and Soybean Meal Price Volatility Pressuring Feed Margins

Raw material price volatility remains a significant challenge to profitability in the beef cattle feed market. Corn and soybean meal constitute 55% to 65% of finishing ration costs, meaning even slight price increases can erode producer margins and constrain spending on premium nutrition products. In March 2026, the geopolitical tensions in the Middle East led to higher diesel, electricity, and shipping costs, further straining feed economics. Additionally, the association noted that the European Union relies on imports for over 95% of its lysine supply and 60% to 70% of its vitamin supply, leaving producers vulnerable to disruptions in Asian supply chains. Rising input costs are already impacting global meat prices. The Food and Agriculture Organization (FAO) beef price index reached a record high in October 2025, up 28% from January 2024 levels. As feed costs escalate, buyers in the beef cattle feed market often delay adopting specialty nutrition solutions and focus on maintaining ration affordability, making grain and oilseed price volatility a persistent margin risk globally.

Additive Approval and Antibiotic-Use Restrictions Slowing Product Rollouts

Regulatory approval for new additives in the beef cattle feed market remains slow and inconsistent. In the European Union, Regulation (EC) 1831/2003 mandates a comprehensive dossier from the European Food Safety Authority before authorization, a process that typically takes 3 to 5 years. This prolonged timeline delays commercialization, particularly for smaller companies with limited regulatory resources, and creates regional disparities in product launch schedules among multinational suppliers. Concurrently, stricter restrictions on antibiotic use are increasing safety and efficacy requirements, thereby raising compliance costs even for established companies. Consequently, the commercialization of differentiated additives continues to lag behind product development in the beef cattle feed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient: Insect Protein Meal Disrupting a Corn-Dominant Value Chain

Corn accounted for 42.5% of the beef cattle feed market size in 2025, maintaining its leading position in finishing rations due to its high energy density and broad availability across North American and South American feedlot systems. Soybean meal remained the primary protein source for high-performance finishing programs using conventional oilseed supplementation. At the same time, Germany’s 2025 monitoring results showed that rapeseed extraction meal could fully support high-performance cattle rations without soy, supporting demand for GMO-free and deforestation-compliant feed options. Wheat and oilseed cakes also continue to serve as important energy and protein inputs, with oilseed cakes gaining attention for lower-carbon ration strategies.

Insect protein meal is projected to grow at a 14.2% CAGR through 2031, making it the fastest-growing ingredient segment in the beef cattle feed market. China’s 2025–2026 feed industry commentary highlighted an increasing focus on insect and single-cell proteins to reduce dependence on soybean meal. However, wider adoption still depends on regulatory approvals in the European Union, Japan, and South Korea. Other ingredients, including urea, distillers’ grains, and agricultural by-products, remain important in cost-sensitive markets, broadening the ingredient mix even as corn retains its dominant position.

By Feed Type: Premixes and Specialty Additives Leading the Next Growth Cycle

Complete feed accounted for 52.0% of the beef cattle feed market share by feed type in 2025, reflecting strong demand for turnkey feeding solutions in large commercial feedlots. Its dominance is driven by lower labor requirements and reduced variability in high-volume finishing operations. Concentrates continue to play an important role in stocker and backgrounding systems, where producers combine them with farm grain, while supplements remain widely used in pasture-based and cow-calf operations that require targeted nutrition.

Premixes and specialty additives are projected to grow at a 6.8% CAGR through 2031, outpacing the overall beef cattle feed market. This trend indicates a gradual shift toward more modular and customized nutrition systems, even as complete feed remains the dominant format. An increasing number of larger operators are acquiring high-performance premix platforms and formulating final rations internally, instead of relying on fully finished feed for every stage. This approach enables feedlots to utilize their own grain more efficiently while expanding direct sales opportunities for additive and premix suppliers in the beef cattle feed market.

By Functional Additive: Rumen-Protected Amino Acids Challenging the Vitamins and Minerals Baseline

Vitamins and minerals accounted for 28.0% of segment revenue in 2025, making them the largest functional additive group in the beef cattle feed market. Their strong position reflects the essential role of macro and trace minerals in supporting growth, immunity, and reproduction across nearly all beef diets. Germany’s cattle-specific mineral feed production increased by 5.5% between 2024 and 2025 to reach 427,000 metric tons in 2025, highlighting stable baseline demand despite herd pressure. Probiotics and yeast are also gaining traction as antibiotic-free programs expand and producers seek more natural performance-support solutions. This trend shows that the beef cattle feed industry is building targeted functionality on top of core nutritional requirements rather than replacing them.

Rumen-protected amino acids are projected to grow at a 9.8% CAGR through 2031, making them the fastest-growing sub-category in this segment of the beef cattle feed market. Their growth is driven by improved metabolizable protein efficiency in high-grain finishing rations, as nutrients bypass rumen degradation and are absorbed in the small intestine. Organic acids and enzymes are also expanding as feedlots aim to improve energy extraction from silage and by-product feeds, supporting wider adoption of advanced additive programs in the beef cattle feed market.

By Form: Pellets Anchor the Market but Liquid Supplements Capture the Growth Premium

Pellets accounted for 46.0% of segment revenue in 2025, establishing them as the leading physical format in the beef cattle feed market. Their prominence is attributed to advantages such as easier handling, uniform density, reduced dust generation, and more precise inclusion rates in both bagged and bulk distribution. Mash remains a cost-effective option for on-farm mixers, while crumbles are particularly beneficial for younger cattle and transition feeding programs.

Liquid supplements are estimated to grow at a CAGR of 8.7% through 2031, making them the fastest-growing segment in the beef cattle feed market. This growth is driven by factors such as self-limiting intake behavior, suitability for remote grazing systems, and the capability to deliver bioactive ingredients without heat damage. In January 2026, Westway Feed Products introduced Synergy with TRT, designed to enhance precision mineral supplementation in beef cattle programs. Challenges such as moisture control and mycotoxin risks remain significant concerns across all feed segments, particularly in humid regions with unreliable storage conditions. Consequently, the selection of feed formats continues to depend heavily on logistics, climate conditions, and nutritional requirements.

Geography Analysis

North America led the global beef cattle feed market, accounting for 33% of revenue in 2025 and the largest share among regions. The United States accounted for significant regional revenue and continued to anchor demand through large feedlot systems and integrated ration management. Beef-on-dairy cattle accounted for 12% to 15% of total United States fed cattle slaughter, underscoring the need for specialized neonatal and finishing nutrition programs. Canada remained the second-largest market in the region, supported by feedlot-intensive finishing in Alberta and export-linked beef production systems. Mexico’s market tightened after the 2025 United States border closure related to screwworm, because more than 1 million retained cattle increased domestic feed demand and lifted cost pressure.

Asia-Pacific is projected to be the fastest-growing region in the beef cattle feed market, with a 5.4% CAGR projected through 2031. In 2025, China was a major country, with its ruminant feed output increasing by 1.8% during the historical period. India is anticipated to be the fastest-growing country market in the region, driven by the increasing adoption of branded compound feeds. Australia and New Zealand benefit from export-oriented beef systems and advanced feeding practices; however, their smaller scale limits their overall contribution to regional revenue growth.

Turkey is a major contributor to market growth, while South Africa, Saudi Arabia, and Egypt are emerging as faster-growing country markets, supported by the adoption of commercial feed and investments in new regional production capacities. European growth in the beef cattle feed market is supported by Farm to Fork environmental policies that encourage methane-reducing additives and stronger animal welfare standards. Western European countries are advancing feed-testing protocols and adopting low-protein diets to meet nitrogen-emission targets. Eastern Europe remains a key growth area as producers modernize operations and integrate with European Union supply chains. Meanwhile, post-Brexit regulatory divergence has increased compliance complexity while also encouraging innovation in ingredient sourcing and formulation flexibility.

Competitive Landscape

The beef cattle feed market in 2025 remained moderately fragmented, with the top five players holding a moderate combined market share. A significant portion of the market was controlled by regional cooperatives, branded specialists, and country-level manufacturers, which competed based on relationships, localized formulations, and service offerings. The primary competitive shift in the market was observed in manufacturing scale, while differentiation increasingly focused on additives, premixes, and nutrition support tools. In September 2025, ADM and Alltech, Inc. finalized their North American feed joint venture agreement. This partnership combined Alltech’s Hubbard Feeds and Masterfeeds with ADM’s 11 US feed mills, expanding their manufacturing footprint across the region. This development highlighted the efforts of large companies to enhance scale in the beef cattle feed market while maintaining strategic separation for higher-value premix and additive operations.

Cargill, Inc. adopted a distinct approach by integrating its nutrition expertise with downstream processing data. This included a USD 90 million investment in its Fort Morgan beef plant and the planned deployment of the CarVe yield measurement system in 2025. Similarly, De Heus Animal Nutrition expanded its operations in India by establishing a new animal feed factory in Punjab, supported by a USD 17 million investment. The facility has an installed capacity of 180,000 metric tons, with the potential to expand to 240,000 metric tons. Nutreco’s 2025 Dutch grant project on nitrogen reduction highlighted the growing importance of research programs focused on environmental compliance as part of competitive strategies in the beef cattle feed market[3]Source: Nutreco, “Nutreco Receives Dutch Grant to Develop On-Farm Solutions to Target Nitrogen Emissions,” Nutreco, nutreco.com. These developments indicate that scale alone is insufficient, as major suppliers are increasingly leveraging data, compliance support, and specialty formulations to maintain their market positions.

Key opportunity areas in the market include low-emission functional formulations, liquid supplement systems for extensive grazing operations, and nutrition solutions tailored to beef-on-dairy calves globally including the United States. Companies that secure early additive approvals and enhance traceability are likely to gain a competitive edge as compliance standards become more stringent across regions.

Beef Cattle Feed Industry Leaders

Cargill, Incorporated

Land O’Lakes (Purina Animal Nutrition)

De Heus Animal Nutrition

Alltech Inc

Archer Daniels Midland

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: De Heus Animal Nutrition opened a new animal feed factory in Rajpura, Punjab, India, a USD 17 million investment with 180,000 metric tons of installed capacity, expandable to 240,000 metric tons, featuring separate production lines for cattle and buffalo, with European automation technology.

- September 2025: ADM and Alltech, Inc. signed the definitive agreement to form their North American animal feed joint venture, with Alltech, Inc. contributing Hubbard Feeds and Masterfeeds, and ADM contributing 11 US feed mills.

- June 2025: Cargill, Inc. announced a USD 90 million investment in its Fort Morgan, Colorado, beef processing plant under the Factory of the Future initiative, including deployment of the proprietary CarVe computer vision system for real-time red meat yield measurement

Global Beef Cattle Feed Market Report Scope

Beef cattle feed is a specialized, nutrient-rich formulation that includes forages (such as pasture, hay, and silage) and concentrates (including grains and protein supplements). It is designed to optimize growth, health, and weight gain in beef production, meeting the nutritional requirements for energy, protein, vitamins, and minerals during both grazing and finishing phases.

The Beef Cattle Feed Market is segmented by ingredient (corn, soybean meal, wheat, oilseed cakes, insect protein meal, and other ingredients), by feed type (complete feed, concentrates, supplements, and premixes and specialty additives), by form (pellets, mash, crumbles, and liquid supplements), by functional additive (amino acids, vitamins and minerals, probiotics and yeast, organic acids and enzymes, and other functional additives), and by geography (North America, South America, Europe, Asia-Pacific, the Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Corn |

| Soybean Meal |

| Wheat |

| Oilseed Cakes |

| Insect Protein Meal |

| Others |

| Pellets |

| Mash |

| Crumbles |

| Liquid Supplements |

| Complete Feed |

| Concentrates |

| Supplements |

| Premixes and Specialty Additives |

| Amino Acids |

| Vitamins and Minerals |

| Probiotics and Yeast |

| Organic Acids and Enzymes |

| Other Functional Additives |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Ingredient | Corn | |

| Soybean Meal | ||

| Wheat | ||

| Oilseed Cakes | ||

| Insect Protein Meal | ||

| Others | ||

| By Form | Pellets | |

| Mash | ||

| Crumbles | ||

| Liquid Supplements | ||

| By Feed Type | Complete Feed | |

| Concentrates | ||

| Supplements | ||

| Premixes and Specialty Additives | ||

| By Functional Additive | Amino Acids | |

| Vitamins and Minerals | ||

| Probiotics and Yeast | ||

| Organic Acids and Enzymes | ||

| Other Functional Additives | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected outlook for beef cattle feed through 2031?

The beef cattle feed market size is projected to reach USD 87.0 billion by 2031 from USD 70.9 billion in 2026, with growth at a 4.2% CAGR over 2026-2031 .

Which region is growing the fastest in beef cattle feed?

Asia-Pacific is projected to be the fastest-growing region with a forecast CAGR of 5.4% through 2031, while North America remained the largest region by revenue in 2025.

What is driving growth in specialty additives for beef cattle?

Antibiotic-free procurement, methane reporting requirements, and precision feeding tools are increasing demand for probiotics, phytogenic, premixes, and rumen-protected amino acids.

Which feed format is expanding the fastest?

Liquid supplements are forecast to grow at 8.7% CAGR through 2031, ahead of other physical forms, even though pellets remained the largest format in 2025 with a 46.0% share.

Page last updated on: